Equinox Partners, L.P. - Q3 2002 Letter

Dear Partners and Friends,

Performance

The acceleration of the global bear market during the quarter was a positive for Equinox, but just barely. During the period, outstanding performance from our short positions offset declines in our Asian and precious metals shares which tracked falling worldwide equity markets. While the recent performance of our long positions and the smaller size of our aggregate short position (now mostly bereft of tech stocks) suggest that the strength of Equinox’s inverse correlation with the global stock markets has waned, the truth is slightly more complicated. Our shorts, of course, remain inversely correlated but have a lower beta than they have had historically. Our longs should perform well in almost any market environment.

The Asian Investment Case: Review and Update

… will continue to be viewed with suspicion by the many asset allocators who still view the asset class as only a high-beta bet on global growth, or a warrant on global trade. Conversely, the region will be viewed more positively by value investors drawn to the region for the relative and absolute bargains on offer. These bargains are best reflected in the availability of high dividend yields.

(Chris Wood CLSA Oct 02).

Chris Wood’s observations may prove more accurate than prescient, as the market has already begun to take notice of the startling dividend yields on offer in .

… Asia will continue to be viewed with suspicion by themany asset allocators who still view the asset class as only a high-beta bet onglobal growth, or a warrant on global trade. Conversely, the region will be viewed more positively by value investorsdrawn to the region for the relative and absolute bargains on offer. These bargains are best reflected in theavailability of high dividend yields.

(ChrisWood CLSA Oct 02).

Chris Wood’s observations may prove more accurate than prescient, as the market has already begun to take notice of the startling dividend yields on offer in .

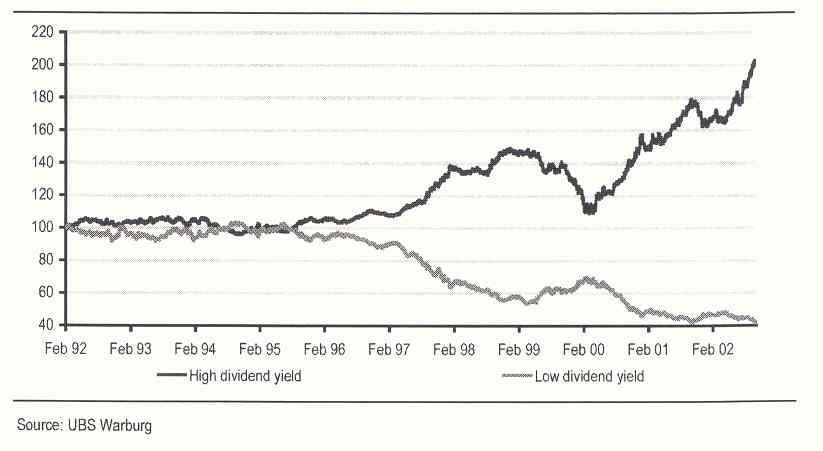

Relative Performance of Asian High-Yield and Low-Yield Stocks

The following table comprised of four Equinox investments in three separate countries makes clear that we have not sacrificed quality for bargain valuations. Our Asian portfolio offers the exceedingly rare combination of high dividend yields, strong balance sheets, and superior returns on shareholders’ equity (ROE’s).

Core ROE as Dividend Yield

Proxy for as Proxy for

Company Quality Company Valuation Company A 59% 4.0%

Company B 29% 5.1%

Company C 21% 13.9%

Company D 19% 5.0%

Despite the meaningful decline in US equities over the last several years, valuations of some of the best American companies remain an order of magnitude richer than the valuations of some of their Asian counterparts. As surely as there are excellent mature branded product companies in America that trade on thirty times earnings, there are outstanding growing branded products companies in Asia trading on three times earnings. This large disparity cannot be justified, only rationalized. Asia’s region-wide vulnerability to Western economic weakness, Korea-specific worries about over-leveraged consumers, and concerns about Indonesia’s security problems are legitimate. But, even if the situation were as dire as it is often portrayed in the financial press, as the saying goes, “It’s (more than) already in the price.”

The current negative buzz surrounding Asian equity markets calls to mind the American sentiment towards the US stock market during the late 1970’s which was famously captured by Business Week’s “Death of Equities” issue. The American investor of that era, by focusing on the past and current woes of American stocks, missed larger positive developments. Likewise, today’s potential investor in Asian securities remains unduly focused on regional economic and market volatility of the recent past. We, however, as long-term value investors, focus on fundamentals not sentiment, and our company specific research has convinced us that Asia’s real progress on multiple fronts transcends these oft-mentioned issues and the short term pessimism they engender.

For example, a view of Asia as simply “a high-beta bet on global growth,” ignores the region’s important shift away from export driven growth to that of local consumption. Those who fear Korean dependency on exports to a vulnerable American economy presumably don’t know that Korea’s exports to China have now surpassed exports to the U.S. China’s impressive development represents a threat to some Asian companies, but its imports have become a region-wide stimulus to economic growth.

The valuations of most Asian stocks imply that significant improvements in corporate governance, especially with respect to capital allocation, have gone unnoticed by much of the world-wide investing class. Our recent visit to Asia revealed that local companies across the region may be on the threshold of a hugely important change in their capital allocation practices. Many expressed a desire to use their burgeoning cash flow more efficiently, which in most cases involves adopting a more rational (i.e. higher) dividend payout ratio. On a trip to Korea and Thailand, we were surprised by the widespread usage of the phrase, “enhance shareholder value,” by managers with whom we spoke. If words actually become deeds, company specific changes in capital allocation policy will have nothing short of spectacular consequences for our extremely undervalued stocks there. To quote a friend and time-tested Korean market observer:

The absolute level of cash holding (at Korean listed companies) should stand at the historically high level, which signifies the fact that slight improvement in the pay-out could lead to sharp increase in the average dividend yield. Korea’s representative company Samsung Electronics mentioned today that they could cancel a portion of treasury shares toward the year-end; meanwhile POSCO decided to retire 3% of shares outstanding as well… more proactive gesture by Korean management properly distributing free cash could likewise induce a re-rating. Koreans tend to follow a trend religiously … Lets hope that the generous distribution of wealth by KSE-listed companies becomes the fashion in Korea. (Victor Kang, ShinYoung Securities Memo 11/26/02)

North American Natural Gas

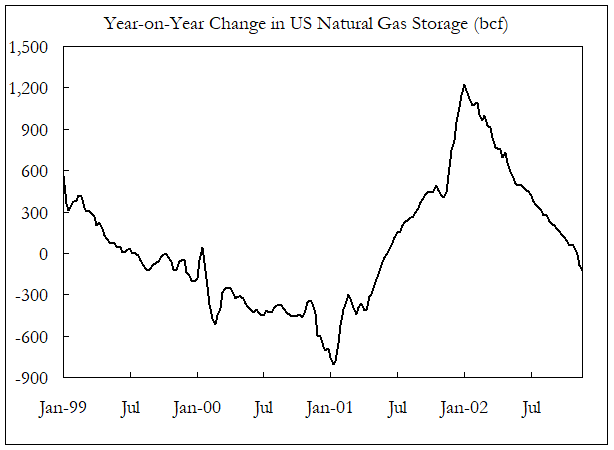

Equinox has significantly increased our exposure to a long-standing theme of ours—North American natural gas. Of late, the supply/demand fundamentals have become increasingly compelling. Specifically, the current dearth of drilling, despite the attractive gas prices, insures that the decline North American natural gas production will continue.

Falling Production Leads to Continued Natural Gas Inventory Declines

Overlaid on the improvement in the North American natural gas market are the increasingly attractive company-specific opportunities we have uncovered. There is a new generation of small Canadian producers with excellent growth prospects and proven management teams. We have added a few of these new names to our group of Canadian energy companies. All of these were purchased at the lowest multiples of next year’s cash flow in memory. Our now large position in gas producing companies means that even non-skiing Equinox investors should wish for a cold winter.

Sincerely,

Sean Fieler

William W. Strong

Anthony R. Campbell