Kuroto Fund, L.P. - Q4 2019 Letter

Dear Partners and Friends,

PERFORMANCE & PORTFOLIO

Kuroto Fund gained +5.8% in the fourth quarter of 2019 and was up +7.2% for the full year. By way of comparison, the EM index was up +11.7% in the fourth quarter and +18.6% for the year.

[1]

We exited two of our top-five positions last year, Aramex and Garanti Bank. The slowing growth of Aramex’s ecommerce business along with a management change tempered our enthusiasm for the company. With respect to Garanti Bank, the doubling of the bank’s stock price made our investment very profitable but less compelling going forward. We trimmed, but did not exit, our holding in Grana y Montero following their dilutive but necessary capital raise last spring. The company remains a sizable position for us but it is no longer a top-five holdings. The three new additions to the fund’s top-five holdings are Logo Yazilim, Georgia Capital, and Guaranty Trust Bank.

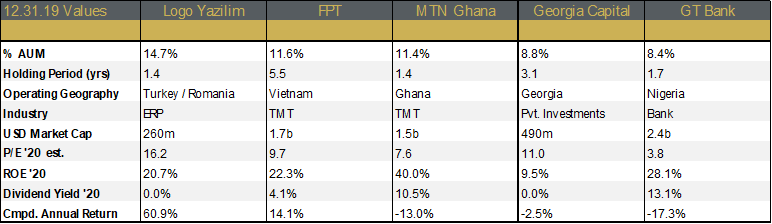

YEAREND top-five holdings

Logo Yazilim

Logo Yazilim is a technology company that provides enterprise resource planning (ERP) software to small and medium sized businesses in Turkey and Romania. As is typical of ERP companies, over half of Logo’s revenues are recurring.

In Turkey, Logo dominates its target market. Amongst small to medium sized businesses using ERP software, Logo’s market share is over 50%. Even more impressively, less than 1% of Logo’s clients switch to a competitor each year. The incredible resiliency of their business was on full display over the past two years as Logo generated strong financial performance throughout Turkey’s economic and political turmoil. Logo’s Romania business, by contrast, is neither as good nor as dominate as their Turkish business. That said, local management in Romania has been making steady progress growing revenues and increasing margins.

Mehmet Tugrul, Logo’s founder, chairman, and 35% owner is responsible for much of Logo’s success. We are particularly impressed with his willingness to engage with other shareholders and his hands-on participation in talent recruitment. Developing world-class software means attracting world-class talent. Tugrul not only understands this but is personally involved in the process.

Given the under-penetration of ERP software with SME clients in Turkey, we expect Logo’s business to grow over 15% per year, with earnings growing over 20%, while generating ROEs over 20%. At 16x 2020 estimated earnings, the shares of this dominant, high-return franchise are still underpriced.

FPT

FPT is a Vietnamese IT outsourcing and broadband company. Through the first 11 months of 2019, FPT recorded 20% revenue growth and 24% growth in profit after tax. FPT’s IT outsourcing business is the company’s principal growth driver, outpacing the company’s domestic broadband business. The company’s IT outsourcing solution continues to take share in Japan and has begun to get traction in the U.S. market as well. The management expects FPT’s outsourcing segment to grow in excess of 20% per year for each of the next three years.

FPT’s management recently broke out a third business line in their financials, education. Years ago, the company entered the higher education business to develop a talent pool for its own IT outsourcing business. That internal business function has now reached scale. At last count, 49,500 students were enrolled in the company’s schools. While FPT’s education segment is still just 6% of the company’s total revenues, we believe it may eventually have significant value as a standalone business. But, even if FPT’s education unit continues to principally serve an internal function, we find it impressive that students are willing to pay to become part of FPT’s core job applicant pool. FPT hires ~40% of the students they graduate.

In recent years, FPT’s chairman and founder, Dr. Truong Gai Binh, has embraced a more streamlined corporate structure as well as more transparent financial reporting. The company’s increased transparency is a direct result of the company’s expansion overseas. FPT’s Japanese and American outsourcing clients want a predictable partner with world-class talent and governance. FPT is delivering on that expectation.

MTN Ghana

MTN Ghana is the dominant telecom and mobile money provider in Ghana. While the company has yet to report fourth quarter results, we estimate that MTN Ghana grew both revenue and earnings over 20% in 2019. This year, we expect the company to pay investors over 80% of its earnings, resulting in an 10.5% dividend yield. More importantly, we believe that, going forward, MTN Ghana will continue to pay out the vast majority of its earnings while maintaining a high growth rate. This particularly desirable combination of a high growth rate and a high payout ratio is made possible by the increasing role of MTN’s capital-light mobile money services.

The value of MTN’s rapid growth and high dividend yield is partially offset by the persistent decline of Ghana’s currency, the cedi. Last year, the cedi declined 11% against the U.S dollar, roughly in line with our expectations given Ghana’s 10% inflation rate. 2020 may be worse, as Ghana’s current president, Nana Akufo-Addo runs for reelection against the country’s former president, John Mahama. We expect more spending and more volatility in the run up to the yearend election results.

While investing in a truly frontier market like Ghana comes with predictable challenges, the dominance of MTN Ghana as well as the quality of its leadership offer the right starting point for such an investment. Selorm Adadevoh, the company’s CEO, is a particularly compelling leader. His TEDx talk gives a taste of his leadership style: watch it here.

Georgia Capital

Georgia Capital is an investment holdings company in the Republic of Georgia. It is run by Irakli Gilauri, the former CEO of the Bank of Georgia and 10% owner of Georgia Capital. Irakli turned Bank of Georgia into one of the best performing banks in the region. He also seeded healthcare and energy startups which turned into large, profitable companies in their own right. Georgia Capital’s broad mandate gives Irakli the freedom to oversee the portfolio of businesses he has helped launch over the past decade in Georgia.

Georgia Capital’s portfolio includes investments in the country’s second largest bank, the largest healthcare company, a water utility, a renewable energy business, a brewery, a winery, an insurance company, an education business, a real estate firm, a hospitality business, and an auto repair business. The bank and the healthcare company are public; combined they cover 78% of Georgia Capital’s market cap. Implicitly, Georgia Capital’s other businesses are severely undervalued given the current price of the holding company. We expect this gap will close as Irakli monetizes several investments in the coming years.

Guaranty Trust Bank

GT Bank is the largest and most profitable bank in Nigeria. The premier financial institution in Nigeria, GT Bank has amongst the lowest cost of funds of any commercial bank in Nigeria. This lower cost of funding allows the bank to generate a 25%+ ROE while taking little lending risk. This low-risk lending strategy, in turn, reinforces GT Bank’s position as the safest commercial bank in Nigeria.

GT Bank’s culture is meaningfully different from every other bank in the country. The difference begins at the top, with Segun Agbaje, the bank’s CEO since 2011. GT Bank’s emphasis on professionalism has allowed it to attract the best talent in-country and executive on its long-run strategic plan. The bank’s superior cost-to-income ratio of 34% captures GT Bank’s focus on both profitability and costs.

The growth opportunities for GT Bank in Nigeria are enormous. Nigeria’s banking penetration is amongst the lowest in the world. We expect GT Bank will grow 15% while earning an ROE of over 25% and paying a dividend yield of over 10% for many years.

Sincerely,

Sean Fieler

END NOTES

[1] Performance stated for Kuroto Fund, L.P. Class A on a net basis. An investor’s performance may differ based on timing of contributions, withdrawals, share class, and participation in new issues. Unless otherwise noted, all company-specific data is derived from internal analysis, company presentations, or Bloomberg. Company valuations and exposures are as of 12.31.19.