Equinox Partners, L.P. - Q4 2025 Letter

Dear Partners and Friends,

PERFORMANCE

Equinox Partners, L.P. rose +17.3% net of fees in the fourth quarter, finishing the calendar year 2025 up +80.9%. By comparison, the S&P 500 index rose +2.7% in the fourth quarter and +17.9% for the year.

Our precious metal miners accounted for the vast majority of our gains last year. Our relatively small exposure to non-commodity Operating Companies in Frontier & Emerging markets also performed extremely well. Our energy equities declined modestly, and our equity shorts were roughly P&L neutral for the year.

Trump's War on the Status Quo

It is no coincidence that our strong performance in 2025 corresponded with the first year of President Trump’s second term. Trump’s frontal assault on the international rules-based order ended decades of coordination between America and Europe, thereby liberating gold and silver from organized government price suppression. Looking ahead to the remainder of Trump’s second term, we expect additional long-dormant market forces to be unleashed as the Western coalition that maintained the post-war economic system breaks down. We also expect America’s unilateral market interventions (such as the current effort to suppress the oil price) to be less successful than the coordinated interventions that characterized the post-World War II era.

The uninterrupted rise in the gold price last year was in large part due to deteriorating relations between the US and Europe. In a break with eighty years of history, at no point did any Western government so much as feign interest in the gold price rally. Neither France, nor Italy, nor the IMF threatened to sell any of their substantial gold reserves. Instead, the gold price suppression scheme run by Western governments for decades simply vanished.

We don’t know if the Trump administration formally decided to abandon America’s policy of gold price management or if the fraught relationship between Europe and the US simply made continued coordination in the gold market impossible. Perhaps Western governments collectively concluded that a gold price suppression scheme had become untenable given the growing list of government gold buyers. Regardless of the cause, the Western government policy of gold price suppression appears to be over.

In a related break with the status quo, Western governments and their financial institutions also stopped managing the silver market. We sense that silver price suppression was never an end in and of itself. Rather, controlling the price of silver was necessary to credibly control the price of gold given the close correlation between the two metals. Accordingly, if the gold market isn’t managed, then neither does the silver market need to be.

It’s unfortunate that Trump has paired his liberation of gold and silver with the enthusiastic suppression of the oil price. This, too, is a break with the status quo. We are aware that for most of the post-war period, America has worked with a coalition of Western oil consuming countries to ensure the long-term availability of oil at reasonable prices. But Trump’s policy of targeting an uneconomic oil price is unprecedented.

Should Trump achieve his stated goal of $50 oil, such a low price will prove unsustainable. With oil averaging $60 over the past year, there has been no increase in US production and non-OPEC supply increases have been muted. Perhaps direct government subsidies can spur a supply increase from Venezuela, but that remains to be seen. Absent new government subsidies, oil production growth will prove a challenge at $60, let alone $50. Harold Hamm, a close Trump confidant, has conveyed this message to Trump. Presumably, Trump realizes his policy of oil price suppression is unsustainable. We certainly do.

While America’s next president may pursue a different policy posture towards Europe, America’s relationship with Europe is forever altered. This change will eventually be reflected institutionally and geopolitically, but its effect can already be seen in the markets. The rising gold price is just one of the first signs of this change. While America’s break up with Europe will at times be unsettling, we expect the resulting changes to be positive for our commodity exposures, as well as our deeply discounted companies in Frontier and Emerging markets.

Investment Thesis Review for our Top 5 Long Positions By portfolio Weight

Solidcore Resources: 11.8% Portfolio Weight

In 2025, Solidcore made significant progress towards cutting its remaining ties to Russia. Notably, they bought back all the shares held in Russian depository and meaningfully advanced the construction of their new Kazakhstan-based POX plant.

With the completion of the Russian share buyback on December 19th, 2025, Solidcore ended a multi-year standoff with Euroclear and created a path to reinstating their dividend. With respect to the POX plant, Solidcore successfully transported their new 1,100-ton autoclave manufactured in Belgium to site in Ertis, Kazakhstan, which was a year-long, technically demanding logistics operation. It required night-time transportation, reinforced roads, and careful coordination to avoid disrupting city life. With the autoclave now in place, the project has begun to ramp full-scale POX construction.

We believe the new POX plant could be up and running by year-end 2027, at which point we would expect Solidcore to re-list their stock on the London Stock Exchange. CEO Vitaly Nesis is working to put in place a world-class board and, along with an LSE-listing, recapture the premium valuation that Polymetal garnered prior to the Russian invasion of Ukraine. It is not often that a CEO gets to build the same company twice, but we think that will be the case for Vitaly Nesis and Solidcore.

The scale of the revaluation opportunity for Solidcore remains mouthwatering. With a current market cap of $3.5 billion, net cash of $1 billion, and annual free cash flow of $1 billion, Solidcore trades at a 2.5x Enterprise Value to FCF (EV/FCF) multiple. Similarly sized peers typically trade at a 10x EV/FCF multiple or more. We think the dividend will be an initial catalyst for revaluation, and the ultimate revaluation will occur when the equity re-lists on the LSE.

Troilus Mining: 10.9% Portfolio Weight

Troilus changed their narrative from "if they" to "when they” go into construction by securing $700 million in project financing in March 2025, which they later upsized to a $1 billion package in November. The $1 billion debt financing covers more than 70% of the project’s $1.3 billion capex. Last December, Troilus raised an additional $175 million of equity, and we expect the $125 million balance of construction cost will be easily financed by selling a royalty on the mine’s by-product metals, such as silver.

On the regulatory and permitting front, in June, the company submitted their Environmental and Social Impact Assessment (ESIA) to the Government of Canada and Government of Quebec. Importantly, government officials have identified the Troilus project as one of the country’s 10 key natural resource developments of interest. Mark Carney even traveled to Berlin with Troilus to sign their offtake agreement, removing any doubt about government support for the project.

This de-risking, both operationally and financially, has positioned Troilus as one of a select few large-scale projects advancing towards construction in Canada. When in production, the Troilus mine will produce an average of 303,000 ounces annually for 22 years at an estimated All-In Sustaining Cost of $1,450 per ounce. When the gold price was $2,000, Troilus was a marginal project in a good jurisdiction. Now with gold trading north of $5,000, Troilus is a high return project in a good jurisdiction. Troilus shares re-rated aggressively in 2025, but the company still only trades at a market capitalization of $650 million, more than a 70% discount to the project’s Net Present Value (using a 5% discount rate and spot metals prices). The mine will be the 5th largest gold mine in Canada, and we anticipate that several large mining companies will have a close look at the project before Troilus makes a final investment decision in December 2026.

Silver Futures: 9.0% Portfolio Weight

Despite the more than three-fold increase in the silver price since January 2024, the supply and demand deficit for the metal hasn’t improved much. Beginning with supply, we expect a de minimis year over year increase in mine supply in 2026 and a 30-million-ounce uptick in recycling. Taken together, we forecast total silver supply will increase 4% in 2026. It’s worth noting that an uptick in recycling is likely a one-time phenomenon, and going forward silver supply growth will depend solely on mine supply. On this point, despite the high silver price, we expect very little mine supply growth again in 2027. Sustained increases in silver mine supply require a more permissive permitting regime in countries such as Mexico, Guatemala, Peru and Chile.

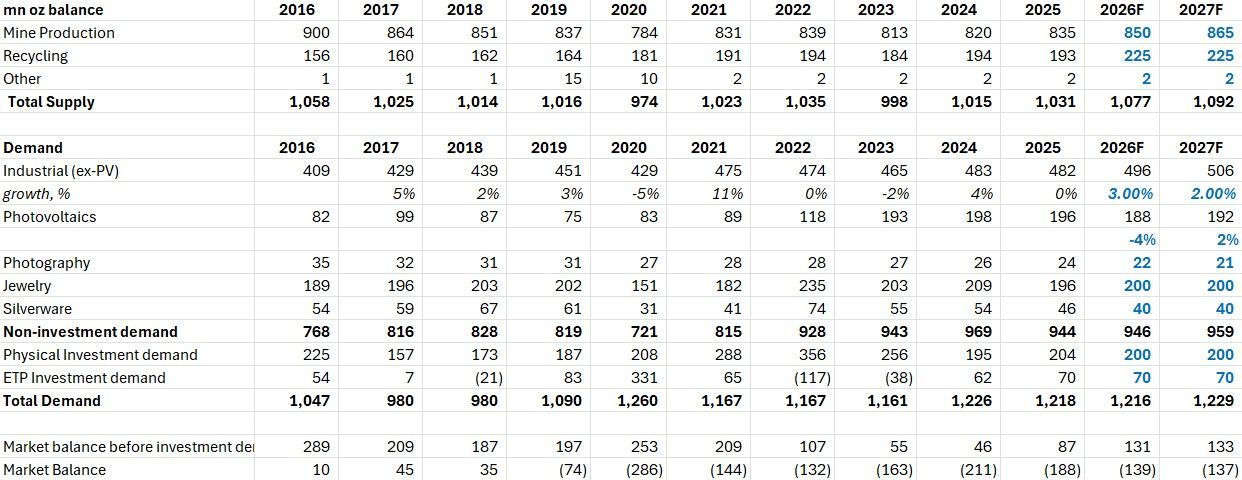

Even at $100 an ounce, we expect industrial demand for silver to remain basically flat. Silver is used in industrial applications because of the unique attributes of its valence electrons, and there is no good substitute in most cases. Absent government restrictions on silver use, we don’t foresee much of a decline in industrial silver demand. The one area of possible demand destruction is in Indian silverware purchases.

Given the inelasticity of both silver supply and demand, we foresee only a modest increase in the metal available for investment to 150 million ounces. (See supply and demand table below) Importantly, a sizable fraction of these 150 million ounces will be consumed by mints producing silver coins. Most incremental investment demand will have to be met by existing owners of metal and the physical silver market will remain tight. We remain bullish, but we’ve trimmed 80% of our silver ounces given the price move.

West African Resources: 7.2% Portfolio Weight

In 2025, West African Resources (WAF) brought their new Kiaka mine into production on time and on budget. Now with two large, low cost and long-lived mines, WAF is the largest and most profitable gold producer in Burkina Faso. We expect WAF to produce more than 470,000 oz per year through 2040.

Unfortunately, the company’s success has not gone unnoticed in cash-strapped Burkina Faso. In September, the government of Burkina Faso expressed their interest in acquiring an additional 35% of the newly completed Kiaka mine as was allowed by the country’s 2022 mining code. As the government does not have the cash to pay for an additional 35%, and the request appears to be an extra-legal attempt to increase the government’s free carry.

The uncertainty caused by the government’s effort to up their stake in the Kiaka mine created a cascade of problems for WAF. Most importantly, their shares were suspended on the Australian stock exchange while the uncertainty was sorted out. While the government of Burkina Faso seems to have lost its enthusiasm for a transaction, WAF still must deal with the overhang and optics of the approach. The result is a particularly cheap stock reflecting the political uncertainty of operating in Burkina Faso.

WAF has an equity market cap of $2.5 billion and will generate close to $1 billion in annual free cash flow. This exceptionally low valuation comes in spite of the long-lived and low-cost high-quality assets the company has put into production. The more recent Kiaka mine has a planned life until 2043 and the Sanbrado mine, which started production in 2020, has a modelled life through 2034 that will likely be extended by several years. The aggregate life of mine All-In Sustaining Costs (AISC) for WAF’s projects are just under $1,700 per ounce, putting WAF into the better half of the global gold mining cost curve.

We expect the uncertainty around the operating environment in Burkina Faso to clarify over the course of 2026 and 2027. The government, at every level, now understands that it receives the majority of the economics of WAF’s gold mines operated in Burkina Faso. Additionally, with gold mining as the chief economic engine for the country, the government’s interests are best served in both the short and long run by encouraging gold mining and extracting their majority share of the economics. Negotiating for more of the economics simply makes it impossible to attract companies to make incremental investments in the country.

Tourmaline Oil: 6.3% Portfolio Weight

We fully exited Tourmaline in January 2026. We have a deep admiration for the executive team that runs Tourmaline, and we agree with the company’s long-term strategy. That said, given the uneven valuation of E&P companies, we believe there are more attractive investments in the sector at this time.

Sincerely,

Equinox Partners Investment Management

[1] Please note that estimated performance has yet to be audited and is subject to revision. Performance figures constitute confidential information and must not be disclosed to third parties. An investor’s performance may differ based on timing of contributions, withdrawals and participation in new issues.

Unless otherwise noted, all company-specific data derived from internal analysis, company presentations, Bloomberg, FactSet or independent sources. Values as of 12.31.25, unless otherwise noted.

This document is not an offer to sell or the solicitation of an offer to buy interests in any product and is being provided for informational purposes only and should not be relied upon as legal, tax or investment advice. An offering of interests will be made only by means of a confidential private offering memorandum and only to qualified investors in jurisdictions where permitted by law.

An investment is speculative and involves a high degree of risk. There is no secondary market for the investor’s interests and none is expected to develop and there may be restrictions on transferring interests. The Investment Advisor has total trading authority. Performance results are net of fees and expenses and reflect the reinvestment of dividends, interest and other earnings.

Prior performance is not necessarily indicative of future results. Any investment in a fund involves the risk of loss. Performance can be volatile and an investor could lose all or a substantial portion of his or her investment.

The information presented herein is current only as of the particular dates specified for such information and is subject to change in future periods without notice.