Kuroto Fund, L.P. - Q4 2018 Letter

Dear Partners and Friends,

PERFORMANCE & PORTFOLIO

Kuroto Fund declined -6.9% in the fourth quarter of 2018 and -17.9% for the full year. The EM index lost -7.6% and -14.5% respectively over the same periods.

[1]

Our poor performance last year was a result of wide spread declines in our holdings. 23 of our 33 investments posted a negative return for the year. Our companies everywhere, even those that delivered strong operating results, declined. For example, FPT, our largest holding, declined 12% in 2018 despite delivering better than expected results. Our companies that delivered poor results declined far more. Most notably, Atento, a top-five position last year, which struggled to just maintain their profitability and replaced their CEO, declined 61% during the year.

portfolio & Fund Size

Our largest client has begun redeeming capital from Kuroto Fund. Over the next twelve months, we anticipate a reduction in the fund’s size to approximately $100m. We will run the resulting smaller fund the same way we’ve run Kuroto for the past decade: ~25 positions with a sizeable amount of our holdings below a market cap of $1b

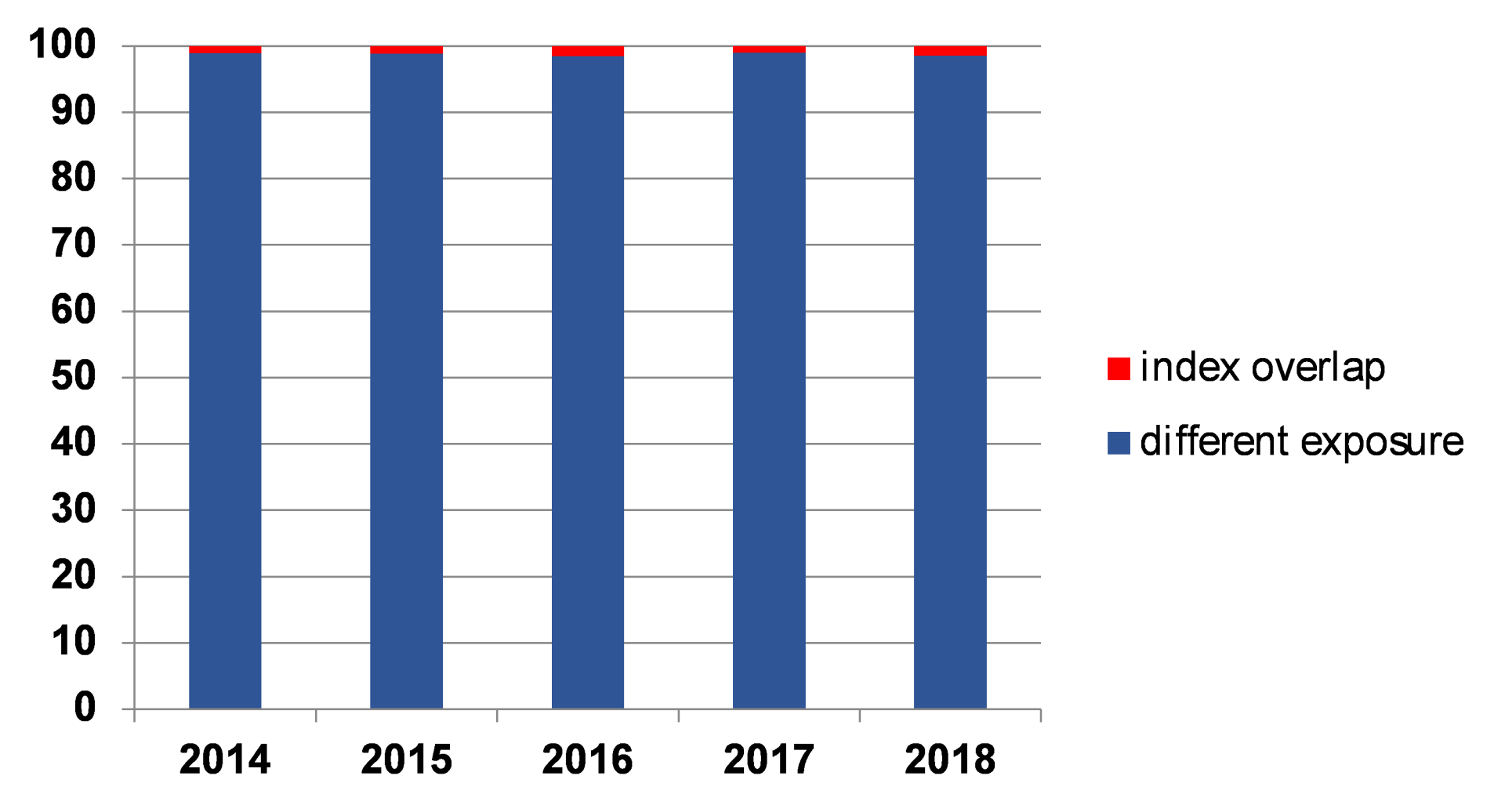

Going forward, we expect Kuroto’s performance to further diverge from the emerging markets index. Our country and company weightings do not even roughly match the index. In fact, Kuroto Fund has an active share of 99% (see graph). In other words, 99% of our portfolio is different than the MSCI EM index.

It is also worth pointing out that our process of identifying superior, undervalued businesses is essentially at odds with the momentum bias of indices, which channel money into large securities irrespective of their fundamentals. The growing concentration of fund flows into indices has obviously been a drag on our short-term performance. Over time, however, this bias in the way indices channel money is generating a growing list of truly superior businesses at increasingly discounted prices.

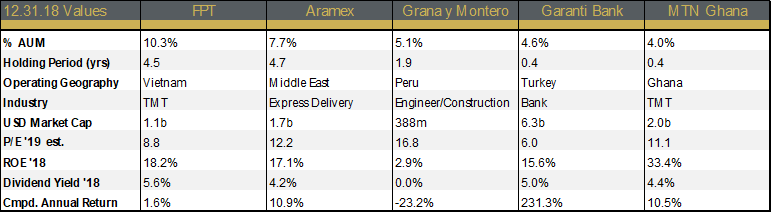

The remainder of this letter highlights the attractive combination of quality, value, and growth found in our top five holdings.

top five holdings

FPT

FPT is a Vietnamese conglomerate consisting of two principal businesses: IT outsourcing and broadband internet.

FPT’s outsourcing clients are mostly foreign, with overseas clients accounting for two-thirds of the division’s revenue. The largest concentration of these clients is in Japan, with Japanese clients currently accounting for a little over half of FPT’s overseas business. While FPT’s IT services are not differentiated from a technical perspective, FPT has trained an unusually large population of Japanese-speaking employees. This language advantage in combination with Vietnam’s low cost labor makes FPT’s offering very competitive globally.

Unlike IT outsourcing, FPT’s broadband business is purely domestic. A member of a three-company oligopoly, FPT generates superior returns and growth by focusing on customer service and bundling their pay TV with a broadband offering. Over the years, FPT has consistently received the best customer reviews in Vietnam and now has almost half of its broadband subscribers choosing to add pay TV to their bundle.

Going forward, we expect FPT to grow their core businesses at a low-teens rate while generating a ~20% ROE. Given the company’s valuations, returns on capital, and dividend yield, FPT is an attractive long-term investment.

Aramex

Aramex is the FedEx of the Middle East.

After promoting their long-serving CFO, Bashar Obeid, to CEO in November 2017, Aramex delivered particularly impressive results. Thanks to the company’s network effect and reputation, the business continued to generate close to a 50% adjusted return on equity (excluding cash and goodwill).

In the first nine months of 2018, Aramex was able to generate 8% revenue growth while walking away from low-margin business in India. This decision to prioritize profit over revenue reflects management’s renewed focus on costs and margins. The financial benefits of this decision were immediately apparent. Margins improved from 10% in 2017 to 12% in 2018. The margin increase led to earnings growth of 25% for the nine-month period, which is well above the high single-digits profit growth we forecasted for the year.

Bashar Obeid also decided to terminate Aramex’s joint venture with Australia Post after a couple years of little progress. While the JV no longer represents a blue sky opportunity for Aramex, the decision reflects management’s disciplined approach to capital allocation and costs.

Grana y Montero

Grana y Montero is the largest engineering and construction company in Peru.

Two years ago, Grana lost their investment in an Odebrecht led concession. This loss left Grana with debt from the concession but not the corresponding asset. This outcome in turn shook the market’s confidence in Grana’s strategy and gave us an opportunity to invest in the company at a substantial discount to liquidation value even with the Odebrecht investment written down to zero.

As we expected, Grana has been able to work through almost all of the issues related to their lost Odebrecht concession. First, they sold hundreds of millions of dollars of assets and used the proceeds to pay off most of the company’s debt. Second, they raised equity to remove the remaining debt overhang. Third, the government specified the maximum fine Grana could face if found guilty of collusion with Odebrecht. Fourth, the company has won new business from private enterprises. Finally, it is increasingly clear that the government will repay Grana for the concession.

On this last point, we expect Grana to collect ~$400 million dollars from the Peruvian government in 2023/2024. Even with the market giving Grana no value for this award, the stock is conservatively worth 50% more than the value for which it is currently trading. And, this 50% rerating assumes no real uptick in infrastructure and mining project spending in Peru.

Garanti Bank

Garanti Bank is the largest and best run private sector bank in Turkey.

In 2018, Garanti Bank performed extraordinarily well despite the ongoing economic turbulence in Turkey. The company began aggressively provisioning for the coming credit cycle and significantly increased credit spreads on new loans. In 2019, we expect Garanti’s profitability to trough at a low-teens return on equity as their cost of risk rises to 2% and their NPL’s peak between 6% and 7% of their loan book.

In 2019, we expect Turkey to present a challenging economic backdrop once again. Specifically, Erdogan’s administration will likely attempt material reforms after the municipal elections in the spring. If the market deems these reforms either insufficient or unorthodox, we could see further weakness in the Turkish lira and higher domestic interest rates. If, however, Turkey gets its macroeconomic policy right, we should see interest rates fall by year-end and a stable Turkish lira. Garanti Bank is well prepared for either scenario and should be in a position to generate returns on equity of close to 20% beginning in 2020.

MTN Ghana

MTN is the dominant cellular telecom and mobile money provider in Ghana.

In Ghana, MTN has over a 50% market share in mobile data and voice and a 94% share in mobile money. The company’s two closest competitors are each individually less than half MTN’s size. MTN’s dominant market share allows them to re-invest more than their competitors, which in turn reinforces their competitive advantage.

We believe that MTN’s mobile money service, MOMO for short, is particularly valuable. The product’s value proposition is obvious. Ghanaians with a MOMO account can earn a better interest rate than they would receive at most banks, purchase incremental minutes directly from MTN, consummate retail transactions, and transfer money to other MOMO account holders. As a result, MOMO account holders have an incredibly sticky relationship with MTN. Over time, as customers use mobile money for more of their daily transactions, we expect that MTN Ghana’s competitive advantages will continue to grow.

organization

As of January 1, our third-party administrator changed from Northern Trust to SEI/Archway. After an extensive search, we chose SEI/Archway due to its combination of culture, use of technology, and competitive fees. Specifically, the Indianapolis-based Archway has low employee turnover, has developed impressive fund accounting software, was recently acquired by global fund administrator SEI, and we negotiated a competitive fee structure. Moving administrators is also a result of the rapid changes in the fund administration business over the last 10 years; we intend to provide our partners with the best service-provider at the best value. Finally, our clients will now be able to access their statements online—directions for doing so are forthcoming in the beginning of February.

Please make note of the contact details for SEI/Archway:

Email: equinox@archwayfo.zendesk.com (this is the preferred method of contact)

SEI AFO

8888 Keystone Crossing, Suite 1400

Indianapolis, IN 46240

Sincerely,

Sean Fieler

Daniel Gittes

END NOTES

[1] Performance stated for Kuroto Fund, L.P. Class A on a net basis. An investor’s performance may differ based on timing of contributions, withdrawals, share class, and participation in new issues. Unless otherwise noted, all company-specific data is derived from internal analysis, company presentations, or Bloomberg. Company valuations and exposures are as of 12.31.18.