Kuroto Fund, L.P. - Q4 2015 Letter

Dear Partners and Friends,

PERFORMANCE & PORTFOLIO

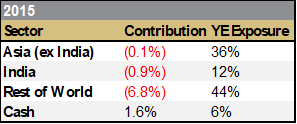

Kuroto Fund increased by +3.4% in the fourth quarter of 2015 and decreased by -8.6% for the full year. By comparison, the MSCI Emerging Markets index rose +0.5% in the fourth quarter and was down -14.8% for the full year. For the year to date through January 28, Kuroto decreased by -5.8% while the EM index began the year down -8.7% over the same period

[1]

2015 was another difficult year for the Kuroto Fund and the fifth year of an emerging markets’ bear market. Following advances in the first four months of 2015, the MSCI EM index declined 24% from April 28 through the end of the year. U.S. dollar strength and China weakness were the biggest drivers of the decline in emerging markets. The effect of weak commodity prices and political upheaval was uneven but also generally negative for the developing world.

While the fund’s performance was certainly disappointing, we believe the quality of the portfolio has vastly improved even though the valuation of the fund did not change over the past year. In the quarter, the fund invested in an Indonesian auto company, a Colombian consumer goods business, a Latin American service company, and a Russian financial. We exited a Mexican insurer, an Indian consumer goods manufacturer, and a Thai service company. These purchases and sales increased the number of companies that the fund owns from 27 to 28.

Our disappointing investment in APR Energy concluded on a similarly frustrating note. Last year, a consortium of Fairfax Financial, ACON Equity Management, and Albright Capital Management effectively partnered with APR’s management in order to recapitalize the company and to take it private at roughly half of its book value. The company’s poorly designed sale process, which we believe failed to appropriately explore all viable alternatives, was particularly galling. Given our experience, it is ironic that Fairfax is a portmanteau of “fair and friendly acquisitions.”

In our opinion, the consortium opportunistically used the company’s violation of its debt covenants as leverage to pursue a deal that was only in the interest of a select few shareholders and management. We, of course, opposed it and voted against it. Unfortunately, not enough other independent shareholders joined us. Therefore, we had no real choice but to sell at the offer price.

The lessons learned from APR are multiple. But, the conclusion once again demonstrated that we not only erred in our assessment of the business and its short-term prospects, but we also erred in our assessment of APR’s management and board. We will redouble our efforts to only partner with superior managements.

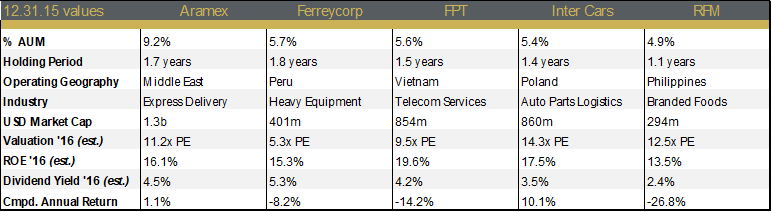

Top-Five Holdings[2]

Aramex

Aramex is a UAE listed express delivery company similar to FedEx or DHL. The combination of the company’s reputable brand and the “network effect” inherent in express delivery forms a particularly durable barrier to entry. Aramex further differentiates itself by its ability to operate efficiently in the Middle East, its entrepreneurial culture, and its variable cost structure.

The company’s financial performance slowed somewhat last year as it revenues increased by 5% and earnings by 11% on a year-to-date basis through Q3. The slower growth was in large part due to currency translation, the lack of growth in Aramex’s freight forwarding business, and the general slowdown in the Middle East as a result of lower oil prices. Freight forwarding, in particular, has suffered from weak demand from oil-related customers and secular changes in its industry. The company’s profitability improved as a result of a mix shift to its higher-margin e-commence business in addition to lower fuel costs.

Despite last year’s slower rate of growth, we believe the company is an extraordinarily attractive investment. We estimate that the company’s adjusted returns on equity (excluding cash and goodwill) are more than 50%, making it one of the highest return businesses we own. The management is world class in every respect. And, importantly, despite two decades of success, the company still has a great long-term growth opportunity as e-commerce further develops in its core markets and as the company expands into new regions. Not surprisingly, Aramex remains our largest single position.

Ferreycorp

Ferreycorp is Caterpillar’s exclusive dealer in Peru since 1942. As we have previously noted, Ferreycorp’s adherence to Caterpillar’s “Seed, Grow, Harvest” business model has allowed it to develop a strong service network. This service network is critical to its mining and construction customers, who need to maximize their equipment “uptime” and can’t afford operational delays caused by equipment failure and downtime. Ferreycorp has a 70% market share in general construction in Peru, 58% in open-pit mining, and 83% in underground mining.

Despite the severe decline in commodity prices and the persistent lack of infrastructure investment in Peru, Ferreycorp was able to increase revenue by 10% and grow its operating profit by 38% on a year-to-date basis through September 30. This strong financial performance is primarily due to the parts and service business which we believe accounted for a majority of the company’s profits last year. In addition, management has instituted several cost-control initiatives over the past twelve months. Finally, even though fewer new mines are breaking ground in Peru, Ferreycorp has benefited from expansions at the existing mines it serves and further gains in market share.

Despite strong financial performance last year, the company’s share price has declined by 24% in USD terms; it currently sells for 76% of its Q3 ’15 book value. Importantly, that book value is largely comprised of liquid, saleable assets. Over time, we believe copper mining and infrastructure investment will grow at healthy rates in Peru and that the company’s parts and service business makes it a more recurring business than the current valuations would indicate. Ferreycorp’s board appears to share this view. They recently authorized the repurchase of 10% of the company’s shares.

FPT

FPT Corp—a Vietnamese conglomerate founded in 1988 by current Chairman, Truong Gia Binh—is a rarity in Vietnam: a sizable corporation that was never state owned. As such, FPT has been able to focus on customer service and returns on capital in a way that is unusual for much of Vietnam. This emphasis has enabled the company to generate a 20% return on equity despite operating a disparate portfolio of businesses. We expect earnings to grow in the mid-teens, which makes FPT significantly undervalued in our opinion at just 9.5x next year’s earnings.

The operating profit of the business breaks down as roughly one-third internet service provider, one-third IT services, and one-quarter retail and distribution of IT products. The small remaining portion of revenues is an assortment of other businesses. As the country’s second largest internet service provider, FPT’s primarily competes against two large state-owned enterprises, VNPT and Viettel. While their respective broadband offerings are roughly equal in quality, FPT has taken share by simply providing better service. Specifically, FPT will both set up new customers and respond to complaints faster. We are optimistic that FPT can preserve this competitive advantage in service and that this business has room for margin improvement as the company upgrades their network from copper wire to fiber optic cable.

FPT additionally provides software outsourcing, system integration, and hardware maintenance. FPT is the largest provider of software solutions to other Vietnamese corporations, and internationally FPT competes with the large global players. Outside of Vietnam, their big advantage is cheaper labor, where they are able to provide services at a 30-40% discount to their Indian competitors.[3] Domestically, FPT has a reputational and, in most cases, technological advantage over the local competition.

Finally, FPT is the largest wholesaler of IT products in Vietnam and is also the second largest distributer of mobile handsets directly to customers. While it took FPT some time to get the retail format right, they are now profitable in that business and benefiting from a shift from mom-and-pop stores towards modern retail.

Inter Cars

Inter Cars is a distributor of aftermarket auto parts in Poland and the Central and Eastern European (CEE) countries. It is the largest player in Poland with a 25% market share and is the fifth largest operator in Europe. Inter Cars inventories and distributes auto parts to independent repair shops. The company’s key differentiators are its speed and availability. Inter Cars sells for 14x its 2016 estimated earnings and has the opportunity to double its business over the next 5 years as it further consolidates the Polish market, expands into neighboring countries, and enters adjacent product categories. The company is run by a sophisticated management team that understands the opportunities and risks to the business.

Repair shops do not have the capital or the desire to stock auto parts. They often do not even know which parts they need until they begin working on a car. They pass on the price of the part to the end customer. And, it is not efficient to seek different parts from different suppliers. As such, repair shops seek a supplier with access to a wide range of parts that can deliver any one of them quickly. Inter Cars understands this and has focused on “widening the offer” for repair shops or offering the highest level of availability and speed. The company’s leading market share in its core markets is a key competitive advantage as this distribution-oriented business model benefits from economies of scale. As Inter Cars stocks more parts, it gets better purchasing terms and has a lower cost of delivery than other players which further cements its competitive position.

Inter Cars has an excellent long-term growth opportunity. The car fleet in Poland and other CEE countries is both old and growing which results in increasing consumption of auto parts. In addition, Inter Cars distributes primarily spare parts today and is only now entering other product categories like tires and lubricants that do not add much incremental costs to distribute. Finally, with roughly 60% of the business still in Poland, Inter Cars has the opportunity to further expand its competitive position in the neighboring CEE countries.

RFM

RFM is a food company based in the Philippines. The company sells for just 12.5x its 2016 earnings, yet has dominant positions in under-penetrated, branded food categories: ice cream (76%) and pasta (39%). RFM was founded by the Concepcion family in 1958 and was initially a producer of flour and related commodity products. The current CEO, Joey Concepcion, has successfully transitioned the company from a family investment arm with several commodity related businesses into more of a branded food and beverage company. Today, 66% of RFM’s sales are branded consumer products with the balance being flour related items.

The company’s ice cream business, Selecta, is a 50/50 joint venture with Unilever, the global market leader in ice cream. Unilever assists with marketing and product innovation, and the two companies have strengthened Selecta’s leading market position through single serve products and a dominant distribution network. Specifically, RFM owns the many thousands of coolers in which the ice cream is stored and leases them out to the retailer. Many of these are in mom and pop stores which co-brand their stored with the Selecta brand name. Given Selecta’s 79% market share in single serve ice cream and 74% in bulk sales, it is difficult for competitors to even gain a foothold at many locations. Moreover, ice cream has a lot of growth potential in the Philippines as less than 1 liter per capita is consumed a year compared with over 18 liters in the United States.

While RFM’s ice cream is clearly their crown jewel, the company has several other strong brands. Management estimates that it has a 39% market share in the pasta category in the Philippines. While rice is the staple food in the Philippines, pasta is increasingly being consumed in the country. The company’s beverage business is a start-up operation that leverages the Selecta brand name for a milk product and licenses the Sunkist brand name for a juice one. Over time, as the branded businesses grow in excess of the flour segment, the company will become a more valuable business. This dynamic, combined with the low penetration in RFM’s product categories and its dominant market positions, will allow for an attractive overall growth opportunity.

Sincerely,

Andrew Ewert

Sean Fieler

Daniel Gittes

William W. Strong

ENDNOTES

[1] Performance stated for Kuroto Fund, L.P. Class A on a net basis. An investor’s performance may differ based on timing of contributions, withdrawals, share class, and participation in new issues. Performance contribution as stated uses the fund’s dollar-weighted gross internal rate-of-return calculations derived from average capital and sector P&L. Sector performance figures are derived using monthly performance contribution calculations in US dollars, gross of all fees and fund expenses. P&L and exposures on bullion, cash, and currency forwards included under Cash. Rest of World is: Brazil, Colombia, Mexico, Peru, Poland, Russia, UAE, U.K. listed EM company.

[2] Unless otherwise noted, all company-specific data derived from internal analysis, company presentations, or Bloomberg. Values as of 12.31.15, unless otherwise noted. Valuations analysis as of 12.30.15.

[3] VPBS, research report, April 15, 2015