Equinox Partners, L.P. - Q3 2022 Letter

Dear Partners and Friends,

PERFORMANCE & PORTFOLIO

In the third quarter of 2022, Equinox Partners, L.P. declined -10.4%. For the year to date through September 30th, the fund gained +3.0%.

Visit our performance page to view the Equinox Partners, L.P. fund summary in more detail.[1]

NATURAL GAS INVESTING : THE Opportunity

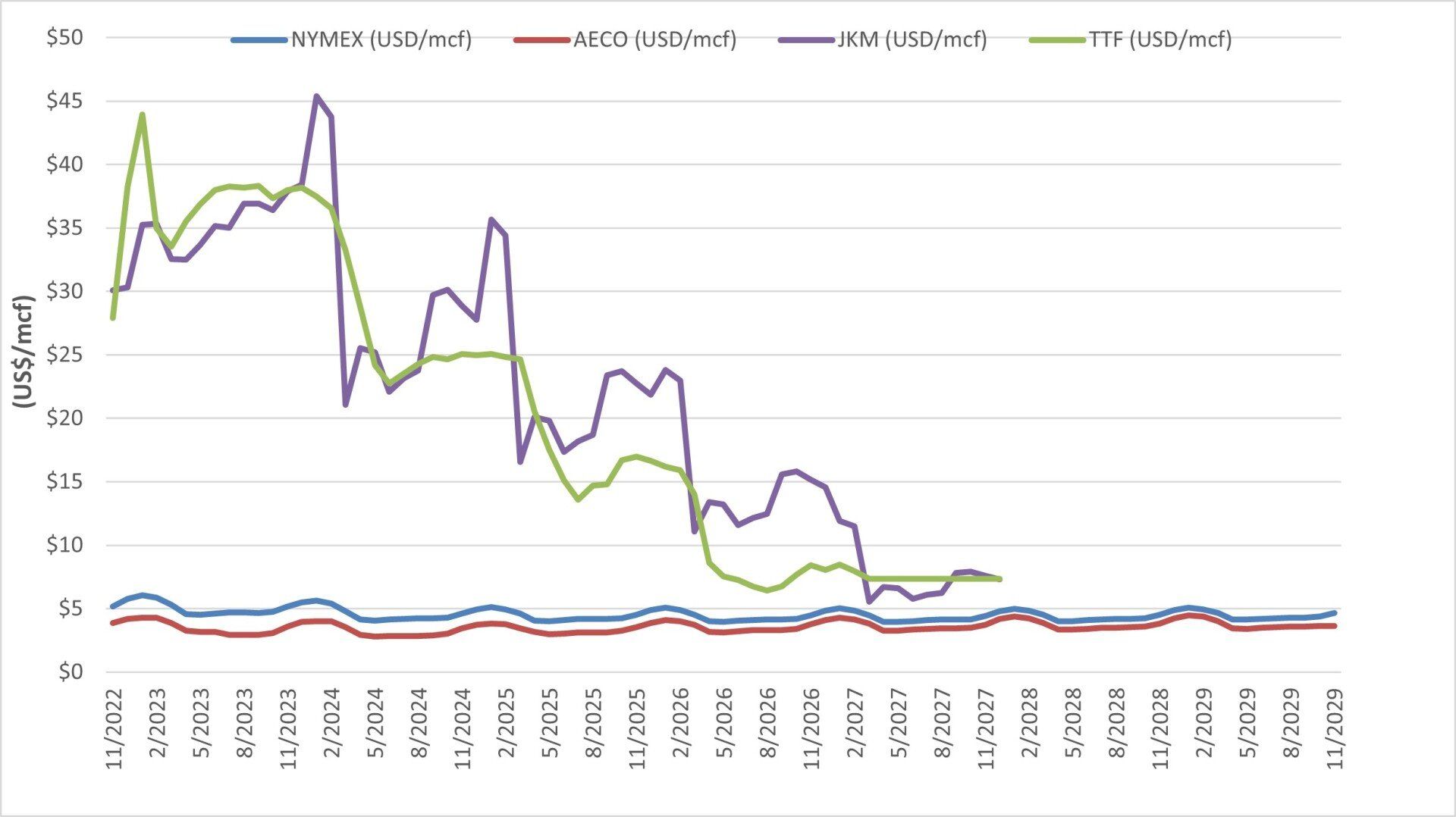

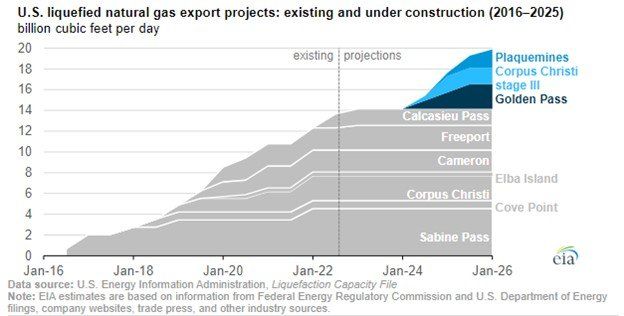

As we write, 1,000 cubic feet of gas (an MCF) trades at $5.60 in North America, $38 in Asia, and $48 in Europe. These massive price disparities are incentivizing unprecedented investments in liquified natural gas (LNG) facilities to move cheap gas from North America to Continental Europe and North Asia. As more gas is liquified and traded across geographies, price disparities should eventually converge on the transportation differential of $5 to $7 per MCF. We believe Equinox Partners, L.P. is positioned to capitalize on this convergence through our ownership of cheap gas in geographies that will realizes higher prices as the LNG market grows.

[letter continues below the Research Room video box]

Watch our Research Room episode on Natural Gas and Crew Energy

The Rub

While the long-term natural gas arbitrage opportunity is clear, the devil is in the details. There are a variety of restrictions that prevent the free movement of gas across geographies. Even within North America, there are long-standing disparities in natural gas prices. Notably, gas in Canada’s Montney and Pennsylvania’s Marcellus have both traded at discounts to the North American natural gas benchmark for years. The mindboggling delays to the Mountain Valley Pipeline (MVP) are a case study in impediments to the transportation of natural gas. Even though the MVP pipeline is commercially attractive and 97% complete, there is no obvious way to complete the project given the environmental opposition. In many cases such political realities make the natural gas arbitrage opportunity more theoretical than real.

The Consensus

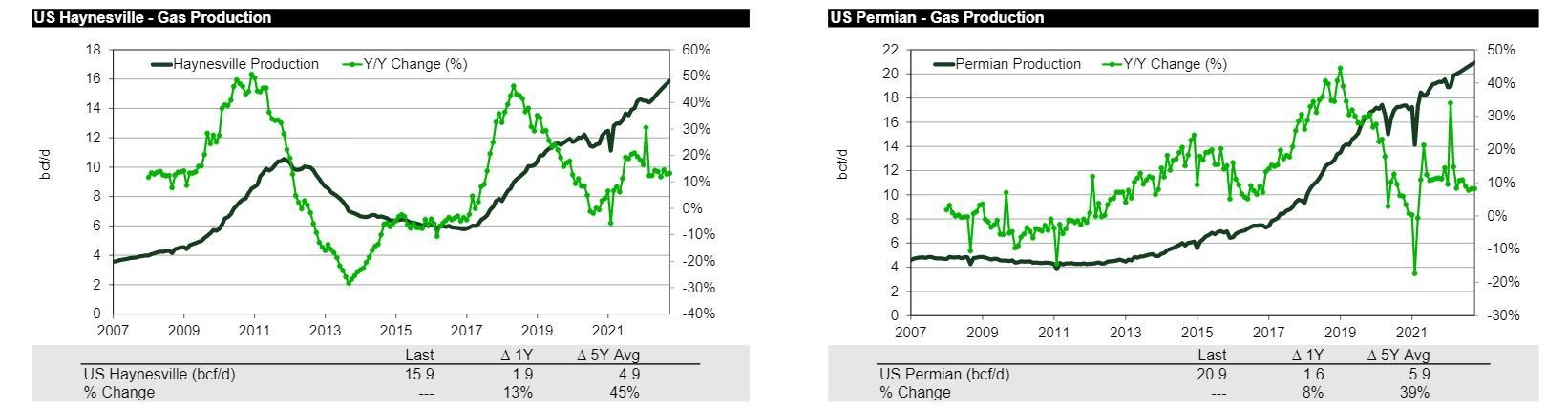

North American natural gas investors have focused on plays with favorable transportation situations. The Haynesville and Permian plays in Louisiana and Texas respectively both fit this bill. They combine attractive geology and a permissive regulatory environment that enables E&P companies to develop these plays at a rapid clip while generally achieving benchmark pricing for their production. As a result of these investments, the Haynesville and Permian have together added over 20bcf a day of production over the past five years. This rapid production growth has even outstripped the growing LNG exports from the Gulf of Mexico, which have increased by 12bcf a day over the past five years.

After years of consistent investment, a growing number of tier-one locations in the Haynesville and Permian have been exploited, and incremental growth potential is limited. As this geological reality plays out, the further growth of North American natural gas production will have to come from prolific fields that have been constrained by transportation issues. In particular, the Montney and the Marcellus will play a larger role in natural gas production going forward. Of these two, we prefer the Montney in Western Canada for two reasons. The play is making clear progress on the long-term transportation issue, and Western Canada’s gas trades at a particularly large discount to Henry Hub.

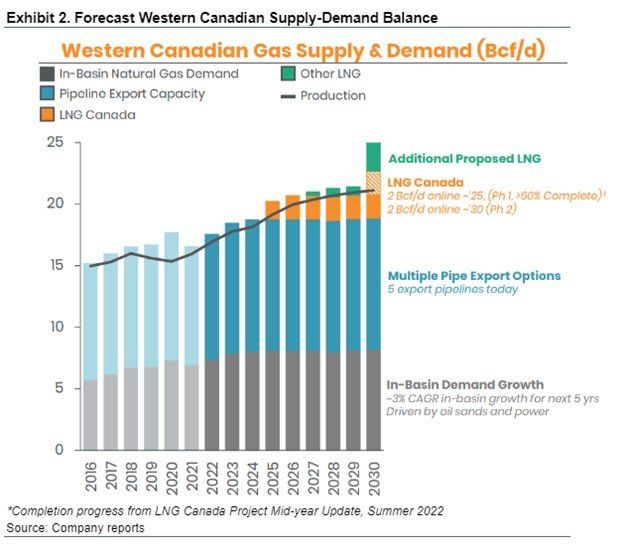

OUR LARGEST INVESTMENT: WESTERN Canadian GAS

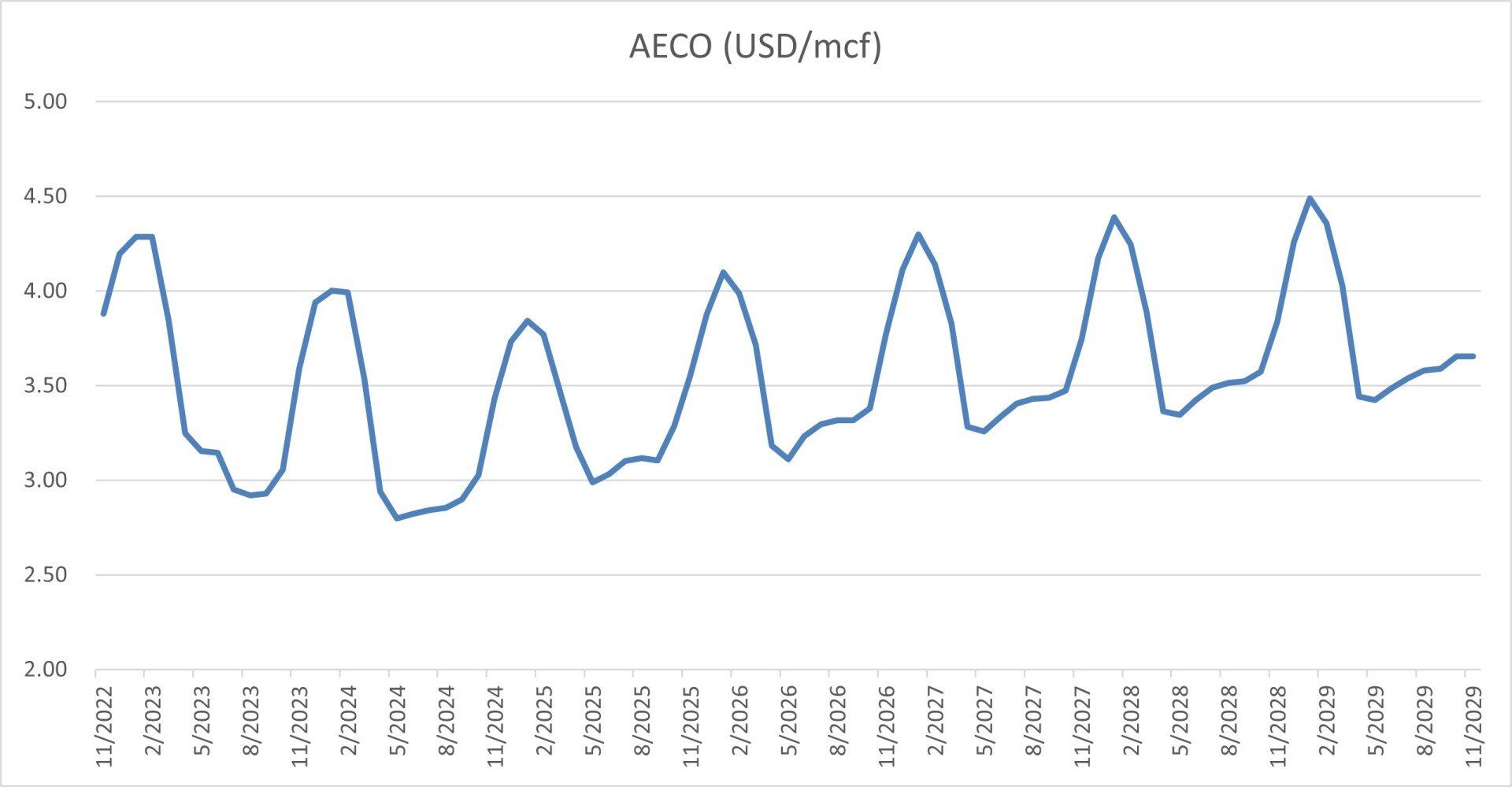

Even though Western Canada has some of the cheapest gas in North America, the futures market is decidedly bearish on its gas. AECO, the Western Canadian benchmark, is projected to average just $3.5USD per MCF over the next five years. That is a 25% discount to Henry Hub natural gas pricing in Louisiana, and an 85% discount to the Asian benchmarks where a growing share of Western Canada’s gas will eventually be exported.

The stock market is equally pessimistic about Western Canadian gas producers. Western Canadian E&P companies trade on low cash-flow multiples that assume low realized natural gas prices. This pessimism is partly attributable to the long-standing problem Western Canadian producers have had getting their gas to market. This historical problem, however, should soon become less relevant as a growing fraction of Western Canada’s gas production is exported to Asia.

With a $29 billion USD price tag, LNG Canada is the most expensive construction project in Canada’s history. The first phase of LNG Canada is projected to come online in April of 2025. The second phase, which will more than double the initial capacity, should be completed by the end of this decade. The $29 billion price tag only covers phase 1. Together, the two phases of this project will result in 4-5bcf per day of additional demand in Canada’s Western Sedimentary Basin. This amount of incremental offtake is significant given that the entire basin’s production is currently 16.5bcf per day. Amazingly, despite the pending increase in demand from LNG Canada, the effect of LNG Canada is not noticeable in the future’s market for gas in Canada nor in the producers' valuations.

LNG Canada consortium members can obtain the incremental gas they need via the drill bit, the spot market, long-term supply contracts, and/or acquisitions. Of these options, the spot market is the least likely given that it entails both price and supply risk. In our opinion, the consortium members will secure the gas they need by growing their own production, entering into long-term supply agreements, and/or making acquisitions. Each of these three strategies has the advantage of allowing LNG Canada consortium members to lock-in their spread for years, if not decades.

To the extent that LNG Canada consortium members will be dependent upon long-term supply contracts and acquisitions, the concentration of the producers of gas in Western Canada makes for some interesting game theory. CNQ and Tourmaline, the two largest producers of gas in Western Canada, produce over 2bcf per day a piece. While these companies could individually meet a sizable portion of the LNG demand, both would be challenging acquisition targets. With market caps of $69 billion USD and $18.5 billion USD respectively, both are too large for all of the LNG Canada participants, except for Shell. Moreover, there is no incentive for either CNQ or Tourmaline to solve LNG Canada’s supply problem without achieving a massive acquisition premium or by improving the overall supply-demand dynamic for gas in Western Canada.

Absent an improbable takeout offer from Shell, CNQ and Tourmaline will work to achieve premium prices on both the gas they contract, as well as the balance of the gas they will continue to sell in Canada’s Western Sedimentary Basin. Accordingly, we believe there is a high likelihood that the Canadian natural gas market could remain tight for a prolonged period and may even eventually trade at a premium to Henry Hub.

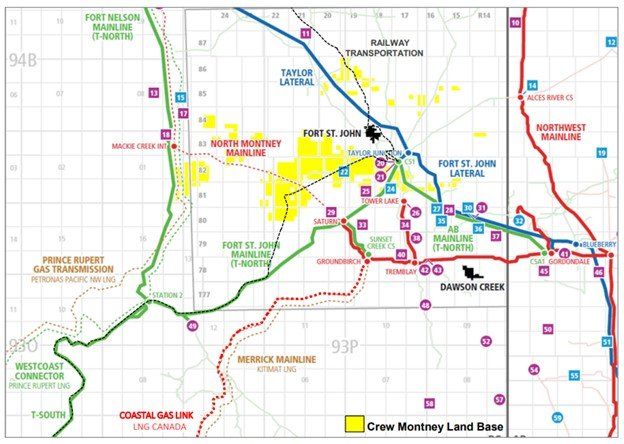

The supply-demand trends in Western Canada make us generally optimistic about the basin and particularly optimistic about our investment in Crew Energy. We project that Crew will be producing 300MCF per day of gas by the time LNG Canada Phase 1 comes online. Importantly, with its large, unexploited land package, Crew can sustain that level of production for more than 20 years. Moreover, Crew’s land package is co-located with LNG Canada’s pipe. This combination of factors makes Crew’s production not just valuable but strategically important. Recognizing the company’s strategic value advantage, unlike many of its peers, Crew has not contracted any of its gas out of the basin after 2025, making all of the company’s gas available for delivery to LNG Canada.

While Crew’s assets merit a premium price, we calculate the company’s upside without a strategic premium, and assume a rerating of the gas price in Western Canada to $5 USD per MCF, Henry Hub’s long-term average. Assuming 300MCF per day of production, $5 USD gas, and a historically normal cash flow multiple of 5x, we believe Crew is worth $3 billion USD. This is four times the company’s current enterprise value of approximately $750 million USD.

Map of Crew’s Land Package in the Montney

Sincerely,

Equinox Partners Investment Management

[1] Sector exposures shown as a percentage of 9.30.22 pre-redemption AUM. Performance contribution is derived in U.S. dollars, gross of fees and fund expenses. Interest rate swaps notional value and P&L are included in Fixed Income. P&L on cash is excluded from the table as are market value exposures for derivatives. Unless otherwise noted, all company data is derived from internal analysis, company presentations, or Bloomberg. All values are as of 12.31.21 unless otherwise noted.

Endnote: Unless otherwise noted, all company-specific data derived from internal analysis, company presentations, Bloomberg, or independent sources. Values as of 9.30.22, unless otherwise noted.

This document is not an offer to sell or the solicitation of an offer to buy interests in any product and is being provided for informational purposes only and should not be relied upon as legal, tax or investment advice. An offering of interests will be made only by means of a confidential private offering memorandum and only to qualified investors in jurisdictions where permitted by law.

An investment is speculative and involves a high degree of risk. There is no secondary market for the investor’s interests and none is expected to develop and there may be restrictions on transferring interests. The Investment Advisor has total trading authority. Performance results are net of fees and expenses and reflect the reinvestment of dividends, interest and other earnings.

Prior performance is not necessarily indicative of future results. Any investment in a fund involves the risk of loss. Performance can be volatile and an investor could lose all or a substantial portion of his or her investment.

The information presented herein is current only as of the particular dates specified for such information, and is subject to change in future periods without notice.