Equinox Partners, L.P. - Q1 2004 Letter

Dear Partners and Friends,

“Weighing Machine” vs. “Voting Machine”: Waiting for a Decoupling

The veracity of Benjamin Graham’s famous dictum that “In the short run the stock market is a voting machine, but in the long run it is a weighing machine,” has been evidenced once again by recent global equity market action. The world over, in the months of April and May, superior liquidity trumped superior fundamentals. As a result, the rapidly growing and very cheap Asian, precious metal and energy stocks which we own and producers of nonrenewable natural resources declined far more than the more liquid but fundamentally inferior U.S. equities that we are shortthe overvalued American tech stocks and over-levered US financial companies which we are short.

It would have been naive to have expected a portfolio that has generated the excellent returns EquinoxEquinox has in recent years to be impervious to sharp corrections. Substantial volatility has always been intrinsic to our strategy. We have chosen to stomach these rapid changes in the value of our fund simply because the fundamentals of the companies we own are so very compelling.

We are not market timers, nor are we macro- strategists. We are stockpickers. Our thorough knowledge of the specific businesses in which we are invested provides us the conviction necessary to stay the course in times like these. This patience has enabled us to be truly long term investors, which in turn has enabled us to generate excess returns over long periods of time Patience, especially in down markets, is a necessity rather than a luxury. Jesse Livermore’s (the legendary stock speculator of the early twentieth century) thoughts on the virtue of patience remain timeless:

“After spending many years on Wall Street and after making and losing millions of dollars I want to tell you this: It never was my thinking that made big money for me. It was my sitting. Got that? My sitting tight!

The reason is that a man may see straight and clearly and yet become impatient or doubtful when the market takes its time about doing as he figures it must do. That is why so many men in Wall Street… lose money. The market does not beat them. They beat themselves, because though they have brains they cannot sit tight.

Disregarding the big trend and trying to jump in and out was fatal to me. Nobody can catch all the fluctuations.” (Edwin Lefevre (Jesse Livermore) Reminiscences of a Stock Operator, John Wiley and Sons, 1923)

Implicit in our preference for stocks with superior fundamentals over those with greater liquidity is the assumption that, over time, the former will significantly outperform the latter. In the short run, investors’ yearning for liquidity has steered them to overvalued equity and debt securities in the U.S. and Europe. In the long run, the compelling combination of valuation and growth that characterizes our longs will carry the day and force them to decouple from their more “mainstream” counterparts. “mainstream” conventional equities. Asian stocks will de-couple from their American counterparts.

A warning to our partners regarding a decoupling: - As should be clear from the global market behavior in the last two months, this divergence we are expecting has yet to begin. When the historic decoupling we are anticipating does come, it is unlikely to develop smoothly. Moreover, we do not expect Equinox’s performance to be immune from the general increase in volatility likely to be brought about by such a significant change in the global market environment.

Equinox: Profiting From U.S. Dollar Vulnerability

“…in recent years our country’s trade deficit has been force-feeding huge amounts of claims on, and ownership in, America to the rest of the world. For a time, foreign appetite for these assets readily absorbed the supply. Late in 2002, however, the world started choking on this diet and the dollar’s value began to slide against major currencies. Even so, prevailing exchange rates will not lead to a material letup in our trade deficit. So whether foreign investors like it or not, they will continue to be flooded with dollars. The consequences of this are anybody’s guess.” (Warren Buffet explaining his ownership of $12 bil worth of foreign currency in his 2003 Berkshire Hathaway report)

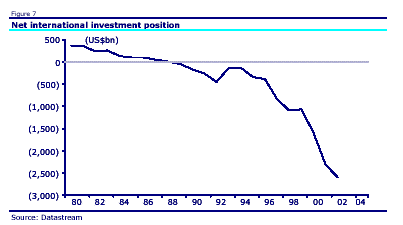

As company specific investors, EquinoxEquinox usually does not hold a view on most currencies. We do, however, hold a long term view on the U.S. Dollar—it is going lower. Despite the almost fifty percent decline of our currency against the Euro in the last few years, America’s current account deficit has yet to peak let alone find a sustainable level. Implicit in the extreme position of America’s external accounts is the possibility of further meaningful dollar weakness. The current global monetary order has long lacked a mechanism to automatically nip unsustainable behavior, such as this, in the bud. This shortcoming, in combination with the surprising willingness of foreigners to hold our currency in extremely large size, has allowed enormous imbalances to persist much longer than we thought possible.

“The international monetary system that evolved after the breakdown of the Bretton Woods system in the early 1970’s is badly flawed. It lacks a mechanism to prevent persistent trade imbalances. It has made it possible for the United States to incur enormous current account deficits totaling a cumulative over $3 trillion since 1980. Those deficits have, in effect, become the font of a new global money supply. This near exponential increase in the global money supply (since the demise of Bretton Woods) has been the most important economic event of the last half-century” (Richard Duncan, The Dollar Crisis, p.251, John Wiley and Sons, 2003)

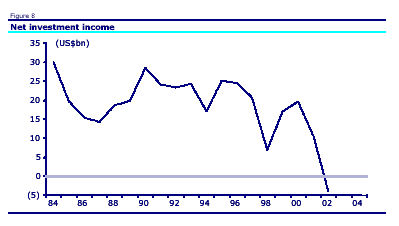

Complacent investors contend that the long running U.S. current account deficit has not yet mattered. While true, as far as it goes, this view fails to address the worsening nature of the problem. Specifically, we are referring to the larger absolute size of our deficit, the rate at which it is expanding, and the compounding effect higher U.S. interest rates will have on the problem. Until 2001 America’s trillion dollar plus net foreign liability cost us less than nothing to finance on a net basis (see net investment income graph[1]).

[1] CLSA Solid Ground: Going For Broke - February 2004

But, with America’s current net foreign investment position deteriorating at a 500bn dollar a year clip, our three plus trillion dollar liability will rapidly create a meaningful annual net investment income outflow.

To make matters (much) worse, if domestic interest rates return to previously “neutral” levels, say 4% - 5%, the implicit effect on the U.S. current account deficit, ceteris paribus, is substantial. The resulting hundred plus billion dollars of incremental interest expense on our global net investment liability would meaningfully exacerbate the effect of our huge trade imbalance. The resulting pressure on America’s net investment position would be considerable and suggests that the dollar remains substantially mispriced. Should current trends continue, our foreign creditors will likely someday decide to not only stop accumulating dollar assets, but actually liquidate those they already own, depressing our currency further. Shorts of US growth and financial companies should likewise be quite profitable.

Each of Equinox’s major investment themes, on a fundamental level, should benefit from the falling value of the U.S. Dollar. In Asia, we own local companies selling local branded products to locals in local currency terms. When Asia’s currencies are eventually allowed to appreciate against the US Dollar (To date, Asia’s local currencies have been held down by the region’s central bankers.), the effect on the vast bulk of our Asian portfolio will be unambiguously positive. Precious metals prices also stand to benefit substantially from dollar weakness, especially any dollar weakness that calls into question the U.S. Dollar’s reserve currency status. Oil and gas prices should, at the margin, be positively affected by a declining dollar. Finally, our short positions in overvalued US equities should benefit from the rise in interest rates likely to accompany dollar weakness. In each of these cases, Equinox’sEquinox’s long portfolio of portfolio is positioned to generate profits larger than those attributable to astute stock picking alone.

Sincerely,

Sean Fieler

William W. Strong